October 2018

DR REQUIER WAIT, head: Economics and Trade, Agri SA and ERIKA DE VILLIERS, head of Tax Policy, South African Institute of Tax Professionals

Diesel is an important input cost for many producers. In terms of agriculture’s total expenditure on intermediate goods and services, fuel represented approximately 9% (R12 billion) in the 2016/2017 financial year.

Diesel is an important input cost for many producers. In terms of agriculture’s total expenditure on intermediate goods and services, fuel represented approximately 9% (R12 billion) in the 2016/2017 financial year.

The diesel refund system supports primary producers in the agriculture, forestry, fishing and mining sectors by giving full or partial relief for the fuel levy and the road accident fund levy. These levies form part of the per litre price of diesel. Businesses involved in qualifying activities can apply to register for the system with SARS and then claim a refund, based on the use (not purchases) of diesel.

The aim of the system is to support the international competitiveness of the agriculture, forestry, fishing and mining sectors. Furthermore, it aims to provide relief from the road related tax burden, for certain non-road users involved in qualifying activities.

According to the Organisation for Economic Co-operation and Development (OECD)’s Producer Support Estimate, the level of subsidies for South African agriculture is amongst the lowest in the world. In this context, the diesel refund is the main support mechanism available to South African producers.

The system was first introduced in 2000, using a phased approach. The administration of the refund system is linked to the VAT system and accordingly, businesses need to be registered for VAT to register for the diesel refund. For this reason, the payment of the diesel refund is linked to other departments within SARS, such as VAT and debtors. Taxpayers need to be cognisant of their net position in terms of VAT and diesel refunds as this has an impact on the processing and payment of diesel refunds. Maintaining detailed records and supporting documents is crucial when claiming a diesel refund.

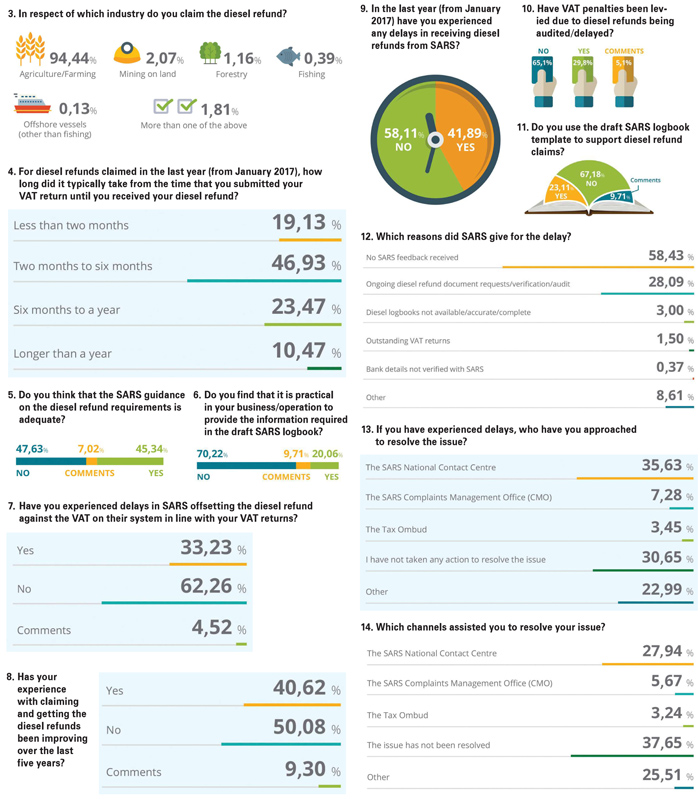

However, complying with the logbook requirements can be problematic. There is uncertainty as to the specific logbook requirements that are used by auditors when auditing diesel refund claims and this can lead to delays in the audit process and payment of the refunds. The diesel refund is conditional in the sense that until a claim has been audited, SARS may cancel a claim that was previously approved.

The diesel refund system is a valued support structure for the qualifying industries, such as agriculture. However, delays in the payment of refunds have an impact on cash flow, leaving a gap in cash flow that needs to be managed.

Emerging farmers, not registered for VAT, cannot currently use the refund system (except for those in the sugar industry). However, the National Treasury and SARS are in the process of reviewing the system and hosted further stakeholder consultations during August 2018. One of the proposals is to separate the administration of the diesel refund and VAT systems.

Within this context, Agri SA and the South African Institute of Tax Professionals (SAIT) collaborated to conduct a survey among users of the diesel refund system. The aim of the survey was to identify any problems experienced with using the current system. The results will be used to engage with SARS on how these issues can be resolved, but also to consider how the proposed new system could help to mitigate and resolve these issues.

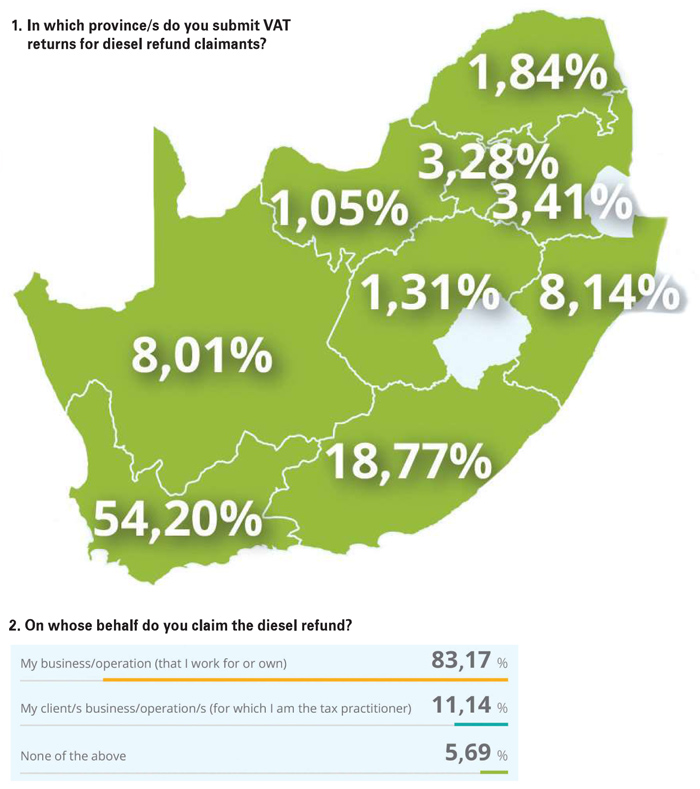

The survey results are summarised in the above infographics. There were 826 respondents of whom 47 did not complete the survey. These respondents were excluded by the control question: On whose behalf do you claim the diesel refund? The 47 respondents do not claim the diesel refund. Accordingly, 779 of the 826 respondents claim the diesel refund. However, note that the results of this survey are indicative of the issues experienced by those who completed the survey. It is not to be generalised as representative of all users that make use of the diesel refund system.

Conclusion

The survey results have highlighted key areas that can be improved. For cases where refunds have been delayed, it seems communication and feedback from SARS is an area of concern. Greater clarity on the requirements and guidelines from SARS is needed – especially in terms of the logbook requirements. Most of the users sampled find the requirements of the draft logbook to be impractical to apply in their business operations.

These results will be shared with SARS, National Treasury and the Tax Ombud, in a spirit of collaboration to resolve current issues and to incorporate solutions in the proposed new system.

Enquiries

Dr Requier Wait, at requier@agrisa.co.za or Erika de Villiers, at edevilliers@thesait.org.za.

Publication: October 2018

Section: On farm level

{kind=link}