Insights shared at a recent media and industry day held by the Animal Feed Manufacturers Association (AFMA) in Pretoria, underscored the extent to which feed manufacturing, grain production, and livestock systems have become structurally interconnected. For grain producers this is a defining feature of demand, value creation, and long-term market stability.

‘The feed industry is embedded within a highly regulated and scientifically driven value chain that begins with grain production and extends through to animal protein on the consumer table. This reality places grain producers in a strategic position as the first link in a system that underpins national food security,’ said AFMA executive director Liesl Breytenbach. ‘The quality, consistency, and reliability of grain production influence not only feed manufacturing efficiency but also regulatory compliance, traceability requirements, and consumer trust in animal-derived food products.’

Breytenbach explained that the formal feed industry operates within one of the most prescriptive regulatory frameworks in agriculture under the Fertilizers, Farm Feeds, Agricultural Remedies and Stock Remedies Act No. 36 of 1947. Within this system, feed ingredients, additives, formulations, and manufacturing processes are controlled before products are allowed into the market. This pre-market regulatory environment places emphasis on prevention and standardisation, with grain forming the primary input into this controlled system.

She contrasted this with much of the retail food sector, where regulatory oversight is more dependent on post-market enforcement and liability mechanisms once products are already in circulation. The implication is that grain entering the feed chain becomes part of a system that is designed for prevention, traceability, and controlled formulation from the outset.

This is of relevance for grain producers as the starting point of the value chain. Their production practices contribute directly to downstream safety outcomes, traceability, integrity, and market access for South African animal protein products.

Understanding feed demand dynamics

According to Petru Fourie, operations manager at AFMA, the feed industry must be understood as a system positioned between grain production and livestock production. She explained that although it is common to focus only on feed manufacturing plants, the reality is that the industry represents a broader value chain that includes raw material suppliers, premix manufacturers, additive providers, and technology partners.

‘We are a smaller value chain within a bigger value chain that operates in the middle between grain producers and livestock producers. This means that grain producers and livestock producers are the two fundamental anchors of the system,’ stated Fourie. ‘Any disruption on either side immediately affects feed availability, pricing, and formulation decisions. The implication for grain producers is that they are part of a dynamic system that responds to livestock cycles, consumer demand, and global market shocks.’

She pointed out that feed demand in South Africa is strongly influenced by livestock production trends. Within AFMA member feed production, poultry remains the dominant driver, with broiler and layer feed together accounting for more than 60% of AFMA’s reported feed volumes. This dominance reflects the efficiency of poultry production systems, shorter production cycles as well as the importance of poultry meat and eggs as affordable protein sources in the consumer market.

Fourie also explained that feed demand closely reflects meat consumption trends. Growth in poultry consumption has driven increased feed demand, while stagnant beef consumption has limited growth in certain feed segments. Egg consumption has grown steadily, and pork consumption has increased through targeted industry development and greater consumer acceptance. These trends highlight the importance of grain producers understanding downstream markets, as changes in consumer behaviour ultimately influence feed demand and grain utilisation.

Industry assurance and shared responsibility

The growing importance of industry assurance systems within the feed value chain was also highlighted. Breytenbach stated that the modern industry assurance systems are becoming increasingly important, not to replace government regulation, but to strengthen traceability, accountability, audit consistency, and consumer confidence. As agricultural value chains become more complex, these systems play a critical role in supporting transparency and maintaining trust throughout the feed and food production system.

To support these objectives, AFMA is currently reviewing its code of conduct for members to introduce a more risk-based and technology-enabled framework. This includes improved electronic auditing systems, enhanced traceability mechanisms, and more consistent reporting structures. The objective is to align industry practices with international standards while reducing duplication in audit processes.

‘As global regulatory requirements become more stringent, the importance of reliable, high-quality grain production will continue to grow. At the same time, sustaining competitiveness, food security, and long-term industry growth will depend on closer alignment and collaboration across the entire feed and food value chain,’ said Breytenbach.

Feed industry shows resilience

Dr Lucius Phaleng, trade adviser at AFMA, said that the feed industry is affected by both global geopolitical disruptions and local factors. ‘International conflicts and supply chain disruptions have increased costs and affected the availability of imported feed inputs, such as essential amino acids, including lysine and methionine, while local logistical and infrastructure challenges continue to place pressure on the feed and grain value chain. While these issues are often discussed in the context of feed manufacturing, they also influence grain markets through substitution effects and changes in formulation economics.’

Despite these challenges, he emphasised the resilience of South Africa’s feed industry. Feed production data for 2025 reflect a recovery of approximately 3,7%, compared to the 6,9 million tons produced in 2024. This recovery has been supported by growth across key livestock industries, particularly the poultry industry, following the disruptions caused by recent avian influenza outbreaks. Broiler feed production recorded renewed growth of approximately 5,1% reaching 3,2 million tons. In addition, the breeder and layer feed segments contributed positively to overall feed output, registering volume growth of 5,7% and 18,1%, respectively.

‘For grain producers, these developments reinforce the importance of understanding the broader feed value chain. Changes in global trade flows, ingredient availability, and feed formulation economics can influence demand patterns for both grain and oilseed products, creating risks but also opportunities for producers who remain responsive to market requirements,’ said Phaleng.

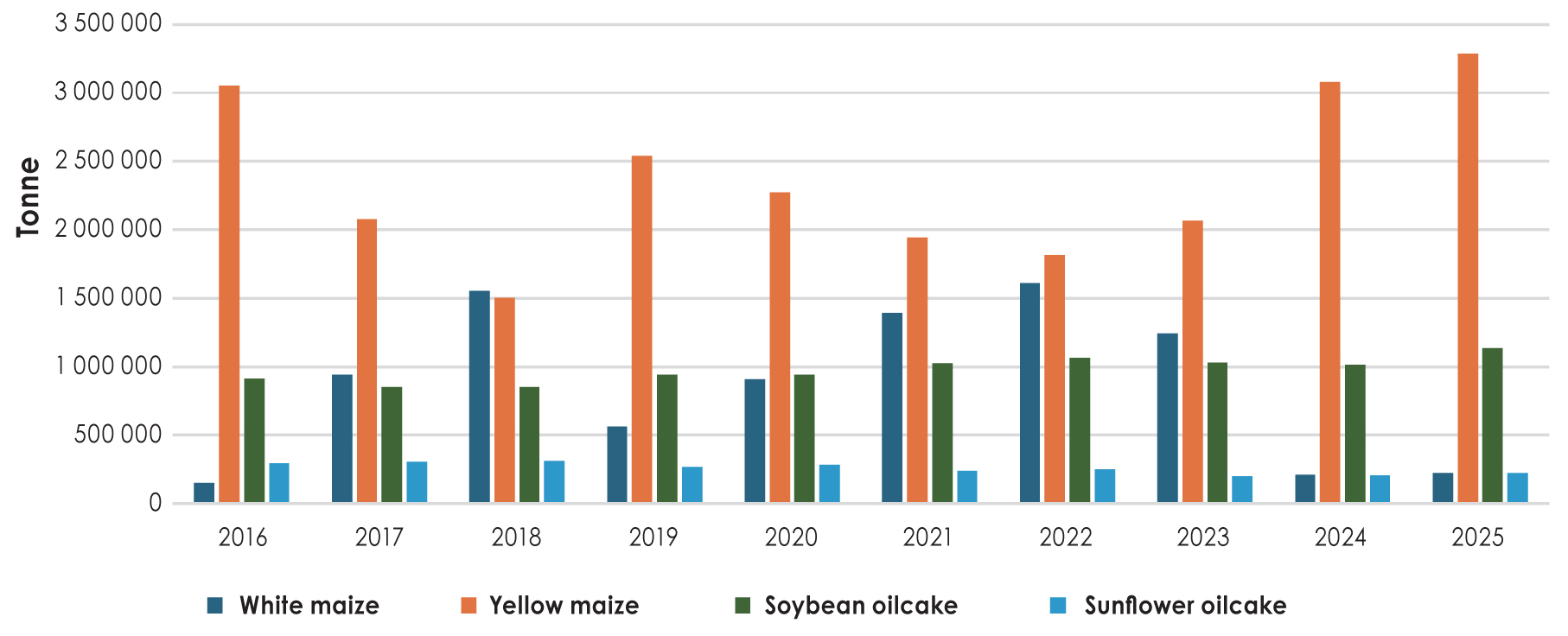

‘Building on this, the structure of animal feed formulation underscores the central role of key raw materials supplied by grain producers. Maize and maize-derived products remain the dominant energy source in compound feed, accounting for more than 53,1% of total feed composition, while oilcake products, primarily soybean and sunflower oilcake, contribute approximately 22,7% as critical protein sources. This composition highlights the strategic importance of grain and oilseed value chains in sustaining the livestock and poultry industries, with direct implications for demand stability and growth.’

Utilisation trends further highlight the strengthening link between feed demand and grain market opportunities.Maize products usage increased from 3,4 million tons in 2024 to 3,6 million tons in 2025, reflecting growth of approximately 5,9%, confirming its continued dominance as the primary energy ingredient in feed rations. Soybean products rose from 1,1 million tons to 1,3 million tons over the same period, representing robust growth of approximately 18,2%, driven by increasing demand for high-protein feed inputs. Sunflower products also increased from 218 000 tons in 2024 to 225 000 tons in 2025, reflecting growth of approximately 3,2%. Collectively, these trends point to sustained expansion in feed raw material consumption, creating meaningful market opportunities for grain and oilseed producers aligned to livestock sector growth.

However, these opportunities remain closely tied to the performance of the animal feed industry. Any slowdown in feed production would directly translate into reduced demand for maize, soybean, and sunflower products, thereby placing downward pressure on grain offtake volumes. Conversely, continued recovery and expansion in feed production will reinforce upward demand pressure, strengthening the market position of grain producers. As feed formulation economics evolve in response to global supply disruptions, input cost volatility, and shifting livestock industry dynamics, the feed industry is expected to remain a key demand anchor for grains and oilseeds, offering both resilience and growth potential for producers positioned across the value chain.

Partnership for growth

Commenting on the AFMA media day, Gerhard Burger, agricultural economist at Grain SA, said that during low producer price market cycles, like the one currently experienced, the interconnectivity between the grain production industry and animal feed manufacturing becomes evident. It is therefore essential that both industries strengthen their relationship and work together to improve technological and financial efficiencies while maintaining and growing their consumer base.

‘Since the animal feed manufacturing value chain heavily depends on grain production and is a main offloading point for grain stocks, Grain SA supports AMFA’s emphasis on enhancing food safety, traceability, and accountability to further build trust in our products,’ stated Burger. ‘Grain SA introduced its own Pest Control Officer (PCO) course to equip members with the necessary knowledge and skills to comply with the provisions of Act No. 36 of 1947 relating to the use of agrochemicals and fertilisers.

‘Although the traceability of grains due to bulk storage, the nature of grain, and the flow of grain stocks throughout the value chain remains a challenge, Grain SA, alongside AFMA, believes that the strength of both the feed and food manufacturing industries relies on the trust consumers place in the products they purchase. We are thus committed to protecting that trust in both the safety and quality of our products,’ said Burger.

{kind=link}