Dr Peter Johnston,

researcher, Climate System Analysis Group, University of Cape Town

Dr Miekie Human,

Dr Miekie Human, research and policy

officer, Grain SA

Steve Arowolo,

PhD student, University

of Cape Town

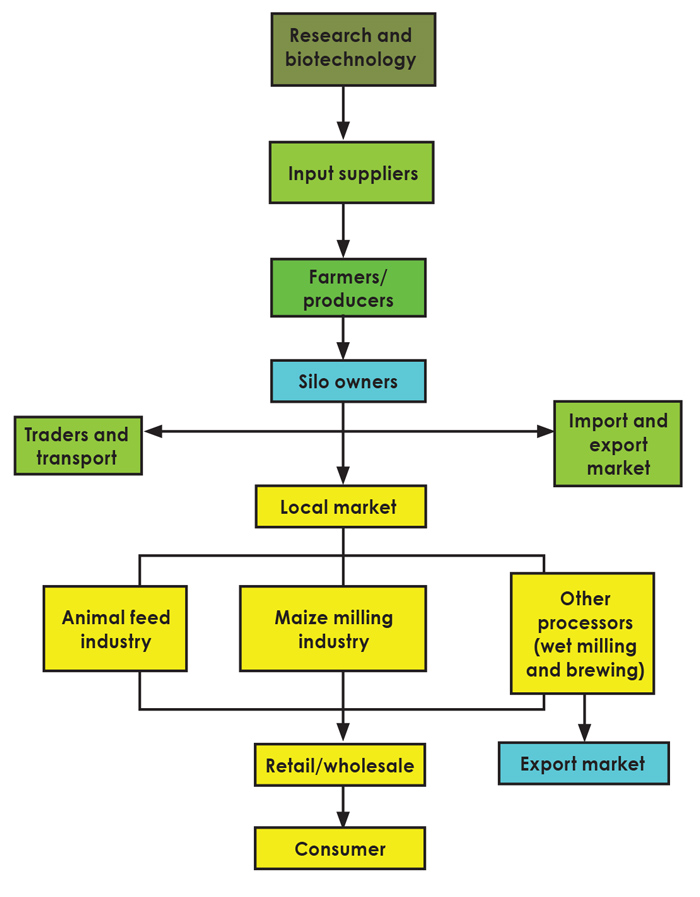

A sustainable and inclusive food value chain is defined as the full range of farms, firms and value-adding activities that transform raw agriculture materials into food products, that are sold to final consumers, in a manner that is profitable throughout the chain, has broad-based benefits for society and does not permanently deplete natural resources.

Climate change

Crop yields are dependent on the amount of heat and rainfall as well as the timing thereof. Decreased or less predictable rainfall will lead to lower yields in many regions, but may allow for higher yields in others. In recent seasons, the effects of erratic rainfall as well as the delayed onset of rainfall have affected a significant proportion of the national maize and wheat crops. For maize, late plantings lead to fewer heat units and the increased vulnerability to frost during ripening. For wheat, late planting leads to poorer germination during colder months and a higher risk of reduced rainfall during grain fill and ripening.

In South Africa, climate change is expected to lead to increases in average temperature of 2,5°C to 3°C by 2050. Increased temperatures will be accompanied by more heatwave days and more very hot days. Nationally, total rainfall is anticipated to decrease, whilst more extreme rainfall events, such as localised flooding and hailstorms, may become commonplace. In summer rainfall regions, decreases of up to 15% have been predicted and in the winter rainfall region, 25%.

The country’s western maize growing regions will experience hotter and drier conditions, which may mean they will no longer be suitable for maize production. Increased temperatures and decreased rainfall may confront the wheat regions of the Western Cape, threatening marginal growing areas.

(Source: Maize Tariff Working Group, 2005)

Pests are also likely to respond to climate change quickly, as the altered environmental conditions enable them to move into areas that were previously unsuitable. Climate change will also affect the incidence of diseases already encountered. Some diseases may become more prevalent and affect the storage industry, as new pests or changes in the incidence of current pests and diseases become likely.

General impacts

Since climate change is likely to result in more extremes, including droughts and floods, it can be expected that variability in climate will similarly result in larger variability of supplies and therefore, more volatility in world markets for agricultural products. This article does not discuss the impacts on the financial aspects of agricultural investment and borrowing.

The components of the food value chain can be grouped according to four main stages, namely production (farming), aggregation (post-harvest handling and food storage), processing and distribution (wholesale and retail). Vulnerability (and adaptation) at farm level has linkages with vulnerability (and adaptation) within the whole grain value chain.

Production

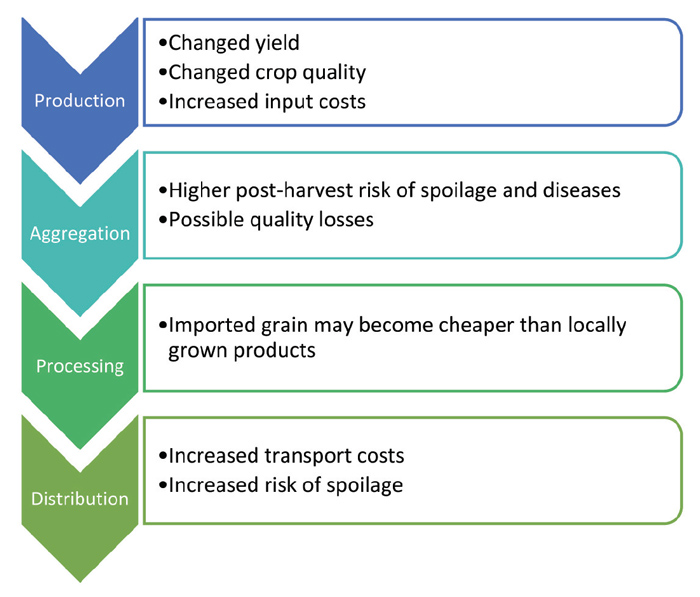

The impacts of a changing and more variable climate lead to three direct impacts: a changed yield, changed quality of the crop, and increased input costs. The most significant linkage between the impacts of climate change at farm level to the rest of the value chain, is reflected in the variable price of the raw grain material. Changes in yield and/or quality in the production of the grain will affect the price (subject to world prices and risks), which in turn will impact on the activities of other participants in the value chain.

Increased input costs make it more difficult to farm grain, leading to smaller areas being planted (though increasing yields are evident), while the number of individual farms may decrease, leading to a reduction in employment numbers. This will have knock-on effects for food security. Seed companies will need to pay attention to developing cultivars better adapted to hotter and drier conditions, while resilient pest and disease management strategies will be crucial to deal with new and existing pests and disease outbreaks. Production practices that ensure optimal yields will be essential.

Aggregation

Transport, storage and trading may be affected by extreme events associated with climate change as well as variability in the form of increased temperatures and heat waves. Higher post-harvest risk of spoilage, disease and quality losses may be encountered, while adjustment from local to imported product will depend on altered transport infrastructure and modalities, with possible increased costs.

The perception of changing climate risk can be enough to influence prices and have upstream and downstream knock-on effects. The indirect linkages of climate risk are also reflected in increased costs of non-grain inputs such as electricity and transport.

Processing

If processing inputs are obtainable on the free market, any increases in the costs of locally produced grain could lead to alternative cheaper supplies being sourced, impacting on local production and employment. If imported grain is not cheaper than locally grown grain, the increased cost of production will be passed on to consumers, conceivably decreasing demand or, in a worst-case scenario in the case of staple crops, causing civil conflict. If free market prices are variable and unpredictable, government subsidies may be necessary to remove large price discrepancies.

Distribution

Distribution risks are likely to increase due to rising transport costs as well as increased risk of spoilage due to increased temperatures and variable, possibly more intense, rainfall. Exports can be threatened by extreme conditions at ports.

Solutions

On a national level, policies to support climate change focus on coordination and cooperation between public and private entities. There are specific actions that can be taken at each stage of the value chain to adapt to the climate impacts.

Climate-resilient crops

More resilient crops that can deliver equal or increased yield and nutrition under future climatic conditions do not come without difficulties. Public acceptability, existing equipment modifications, lack of knowledge, and marketing challenges are some of these.

Collaboration between breeders, physiologists and climate scientists is needed to expand the natural and genetic variability of existing grains for heat and drought stress. Crop physiology studies need to investigate responses under future climatic conditions, such as changes to temperatures, rainfall, carbon dioxide levels and altered planting windows.

Breeding approaches to create drought- and heat-tolerant grain cultivars for South African producers ought to expand genetic variability by incorporating drought- and heat-resistant germplasm from alternative sources, or induce random mutations and identify beneficial changes that can be adopted. Crop physiology studies should observe and test drought and heat responses under future climatic conditions with increased CO2 levels, changing rainfall and increasing temperatures.

Research should also evaluate the responses of commercial cultivars when grain is planted outside the optimal planting window to determine optimal regions for grain cultivars under a changed climate regime. Ways in which management practices can be adapted to minimise expected impacts must also receive attention.

Sustainable agricultural practices

Climate risk studies can assist producers to manage climate risks (drought/increased temperatures) to minimise the expected impacts. Increasing climate resilience has shown to be possible through adopting sustainable agricultural practices that focus on optimal soil and water management as the departure point, and then integrating crop science and management decisions to optimise resilience to extreme conditions. Many examples of success with minimal till, cover cropping, legume rotation, ecological pest management, and integrated livestock systems have been recorded.

The costs of sustainable and conservation agriculture approaches may initially require greater capital expenses, but are expected to be rewarded by increased returns through improved soil moisture and fertility, and reduction in pests.

Value chain resilience

Climate change will affect the entire grain value chain. For silo owners, storage practices will have to be reviewed and amended to limit incidence of ’new’ pests and diseases in stored grain. Where regions become unsuitable for the production of a particular crop, adaptations will have to be made. Changing crop production will ultimately impact on exports and associated markets.

The impact of climate change on the value chains of specific products from specific countries will not be identical. In countries or regions where climate change may have a positive impact on grain production through beneficial changes, it should result in a positive feedback on the value chain and vice versa.

Positive and negative impacts on the cost of production may influence the price which producers obtain for their product, but the ruling market prices are influenced by many local and international factors. If climate factors increase the cost of production of grain in South Africa, for example, but the price on the international market is not affected, it will have a negative impact on actors involved in production and aggregation, but not necessarily in processing or distribution.

An improved understanding of climate change impacts will enable us to build resilience to climate change, while developing human and technological capacity to respond to these impacts. It is clear that the grain industry will need to increase its resilience through the entire value chain in order to survive these threats. Further research and collaboration are essential.

{kind=link}