Juan-Pierre Kotzé, manager: Research and Projects, SACOTA

Juan-Pierre Kotzé, manager: Research and Projects, SACOTA2026/06/23

THE ROLE OF INVESTMENT FUNDS IN THE COMMODITY DERIVATIVES MARKET (CDM) OF THE JSE REMAINS A DEBATED TOPIC IN THE SOUTH AFRICAN GRAIN INDUSTRY. OPINIONS VARY WIDELY. SOME MARKET PARTICIPANTS BELIEVE FUNDS CONTRIBUTE TO EXCESSIVE PRICE MOVEMENTS, WHILE OTHERS ARGUE THAT THEY PLAY AN IMPORTANT ROLE IN PROVIDING LIQUIDITY TO THE MARKET.

The reality, however, is that without access to adequate information about the positions held by different categories of market participants, it is impossible to accurately determine the extent of the influence that funds may have on commodity prices.

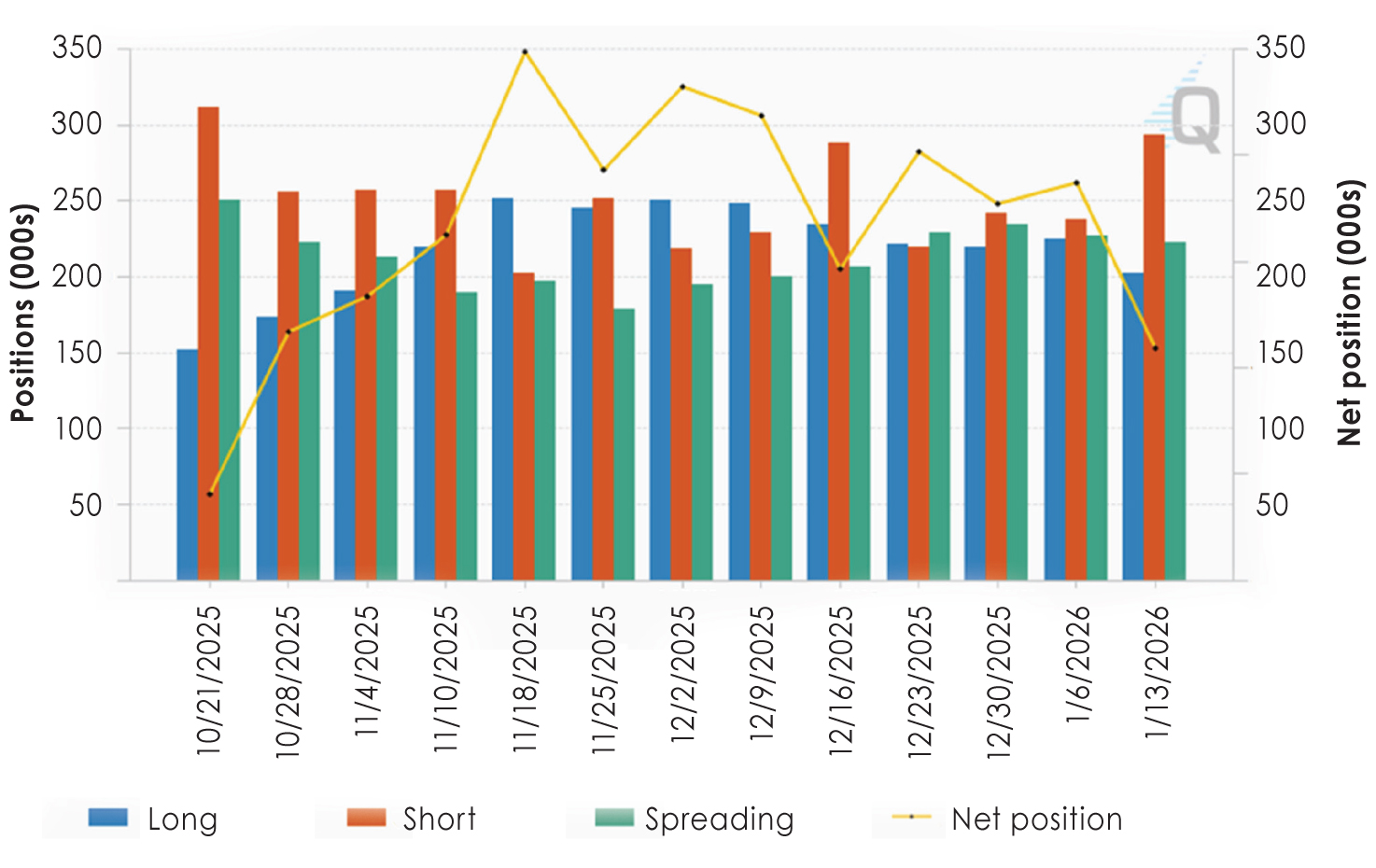

The predecessor to the current CME Group, the Chicago Board of Trade (CBOT) already started publishing position reports in June 1962. However, versions of this report can be traced back to as early as 1924 when the US Department of Agriculture’s Grain Futures Administration regularly started publishing such information. Today it is generally known as the Commitment of Traders (COT) report.

Agricultural commodity prices are naturally volatile. Seasonal production variations, weather events, exchange rate movements, global supply and demand dynamics, logistics constraints, stock levels, and food security concerns all contribute to price fluctuations.

Questions often arise when price movements appear more intense or more prolonged than what market participants believe can be justified by underlying market conditions alone. A notable example was the movement in the JSE CDM white maize price from May to mid-July 2025 when prices increased by approximately 21% only to decline by roughly 27% over the next month and a half. Although there were market concerns regarding weather conditions and crop estimates at the time, many participants questioned whether these factors alone explained the magnitude of the price movements. The challenge is that nobody can answer this question with certainty because the market does not have access to sufficient information regarding the positions held by different categories of participants.

Among traders, there are differing opinions regarding the role played by investment funds in the commodity derivatives market. Some market participants believe that many funds make extensive use of algorithmic trading systems. These algorithms often rely on technical indicators, momentum signals, and trend-following strategies. In simple terms, they tend to buy when markets are rising and sell when markets are falling. According to this view, algorithmic trading (algo-trading) does not necessarily manipulate the market. Rather, it responds to market signals and trends that are already present.

Traditionally, by buying and selling based on research analysis and forward market views, funds added liquidity and absorbed some of the short-term shocks that could otherwise result in abrupt and disorderly price movements. However, this is not necessarily the case anymore. Critics of algo-trading contend that trend-following algorithms can sometimes keep prices elevated for longer than fundamental conditions would justify, or alternatively, keep prices under pressure longer than expected.

The problem is that these remain opinions rather than facts. Without reliable information regarding the actual positions held by funds and other market participants, it is difficult to distinguish between perception and reality.

Importance of a COT report

SACOTA (South African Cereals and Oilseeds Trade Association) and other industry participants, including Grain SA, have requested that the JSE publish a COT-type report like those available on major international commodity exchanges, particularly in the United States. A COT report categorises market participants according to their role or type of positions in the market and reports their aggregate positions. For example, it may distinguish between:

- hedgers such as producers, grain traders, processors, and users;

- managed money or investment funds; and

- other speculators and investors, e.g. spread traders.

Such information does not disclose individual positions but rather provides an aggregated view of market participation, and changes over time. The latter is an important indicator and are often compared to price trends.

This allows market participants to understand who is driving market activity. If managed money holds a large net long position, one may infer that investment funds expect prices to strengthen. Conversely, if hedgers as a group hold significant long positions, it may indicate that the physical market believes current prices represent value and could increase. Similarly, if producers, traders, and processors are collectively increasing their short positions, it may suggest expectations of, for example, greater supply or lower future prices. Such insights help market participants make more informed decisions and improve the overall price discovery process.

Importantly, a COT report would not necessarily prove whether funds are causing prices to rise or fall. Rather, it would provide the information required to have an informed discussion based on facts instead of speculation. Markets function best when participants have equal access to reliable information. A COT report is only one component of a transparent market. Information relating to, for example, stock levels, product quality, accessibility of inventories, out-loading rates, and logistics also plays an important role. However, data on open-interest position categories remain a significant missing piece ofthe puzzle.

Internationally, exchanges such as the CME Group and ICE Futures in the United States publish COT reports that have become an important tool for traders, producers, processors, and analysts. These reports allow market participants to understand whether price movements are being driven primarily by hedgers or by investment capital. Important to note, data are often collected and released (published) by a government body. The exchanges would then compile and publish their own reports. For example, the US Commodity Futures Trading Commission (CFTC) compiles and publishes the official data. However, it differs from country to country. Examples of other global exchanges that publish similar reports include Euronext Commodities and the London Metal Exchange (LME). In Asia, the Tokyo Commodity Exchange and the Shanghai Futures Exchange provide their own open-interest and large position data reports although the format differs slightly from the US legacy format.

The industry’s request for a COT report has been discussed with both the JSE and the Financial Sector Conduct Authority (FSCA). The JSE’s position has been that current legislation and exchange rules do not permit them to publish participant information, even in aggregated form, without the consent of the participants concerned. The FSCA has similarly indicated that the Financial Markets Act does not currently provide it with the authority to compel or authorise the publication of such a report. The act is presently under review, but any legislative changes could still take several years.

However, recent developments may have opened new avenues for obtaining greater transparency. In January 2026, the Information Regulator issued an enforcement notice relating to a separate information request directed at the JSE under the Promotion of Access to Information Act (PAIA). The ruling reaffirmed the importance of transparency and indicated that confidentiality agreements do not automatically override the right of access to information where legislation permits disclosure. (The JSE did indicate they will appeal the outcome in court.) While the matter did not specifically concern a COT report, it has renewed debate regarding what information may potentially be disclosed under South African law and whether alternative legal mechanisms could be used to obtain aggregated trading data.

The JSE does publish daily market data products through the JSE Marketplace data shop, with some reports distinguishing between local and foreign positions. Unfortunately, they do not publish any commodities data or category of positions (open interest).

As a result, SACOTA continues to explore several possible avenues, including engagement with National Treasury, the Minister of Agriculture through the National Agricultural Marketing Council (NAMC), and the Competition Commission as well as using potential processes available under PAIA.

Ultimately, the debate is less about whether investment funds help or hinder the market, and more about the lack of transparency. Improved market reporting, such as a COT report, would provide the insight required to support informed decisions, strengthen price discovery, and enhance confidence in the JSE commodity derivatives market.

{kind=link}