senior landbou-ekonoom,

Graan SA

Gerhard Burger, junior agricultural economist, Grain SA

Gerhard Burger, junior agricultural economist, Grain SA Gerrit Olivier, agricultural economist intern, Grain SA

Gerrit Olivier, agricultural economist intern, Grain SAAGRICULTURAL INPUTS SUCH AS FERTILISER, LIME, AND GYPSUM PLAY AN IMPORTANT ROLE IN GRAIN PRODUCTION. HOWEVER, THE PRICES OF THESE INPUTS ARE INFLUENCED BY A COMPLEX COMBINATION OF GLOBAL COMMODITY MARKETS, ENERGY COSTS, EXCHANGE RATES, AND SUPPLY CHAIN CONDITIONS. UNDERSTANDING THESE MARKET FORCES HELPS EXPLAIN WHY INPUT COSTS CAN CHANGE SIGNIFICANTLY FROM ONE MONTH TO THE NEXT.

Over the past few months, international markets have experienced considerable volatility as geopolitical tensions disrupted global trade and fertiliser supply chains. Although conditions are beginning to stabilise, uncertainty around sulphur supplies, shipping routes, and currency movements continues to influence local prices. At the same time, purchasing quality fertiliser and lime remains just as important as monitoring prices, ensuring producers receive the full value from these essential production inputs.

Global energy markets remain the foundation of fertiliser prices

Most fertilisers begin with energy. Natural gas is the primary raw material used to produce ammonia, which forms the foundation of nearly all nitrogen fertilisers, including urea and LAN. At the same time, crude oil refining produces sulphur, which is converted into sulphuric acid, a critical ingredient in the manufacture of phosphate fertilisers such as MAP and DAP.

This means that whenever global oil or natural gas prices increase, fertiliser production costs usually follow. For South Africa, the impact is even greater because more than 80% of the country’s fertiliser raw materials and intermediates are imported. Local fertiliser prices therefore depend heavily on international energy markets, shipping costs, exchange rates, and global supply chain conditions.

Over the past few months, geopolitical tensions in the Middle East have demonstrated just how quickly international events can affect agricultural input costs. The conflict surrounding the Strait of Hormuz disrupted one of the world’s most important shipping routes for crude oil, natural gas, ammonia, sulphur, and fertiliser products. As uncertainty around supply increased, international fertiliser prices responded almost immediately.

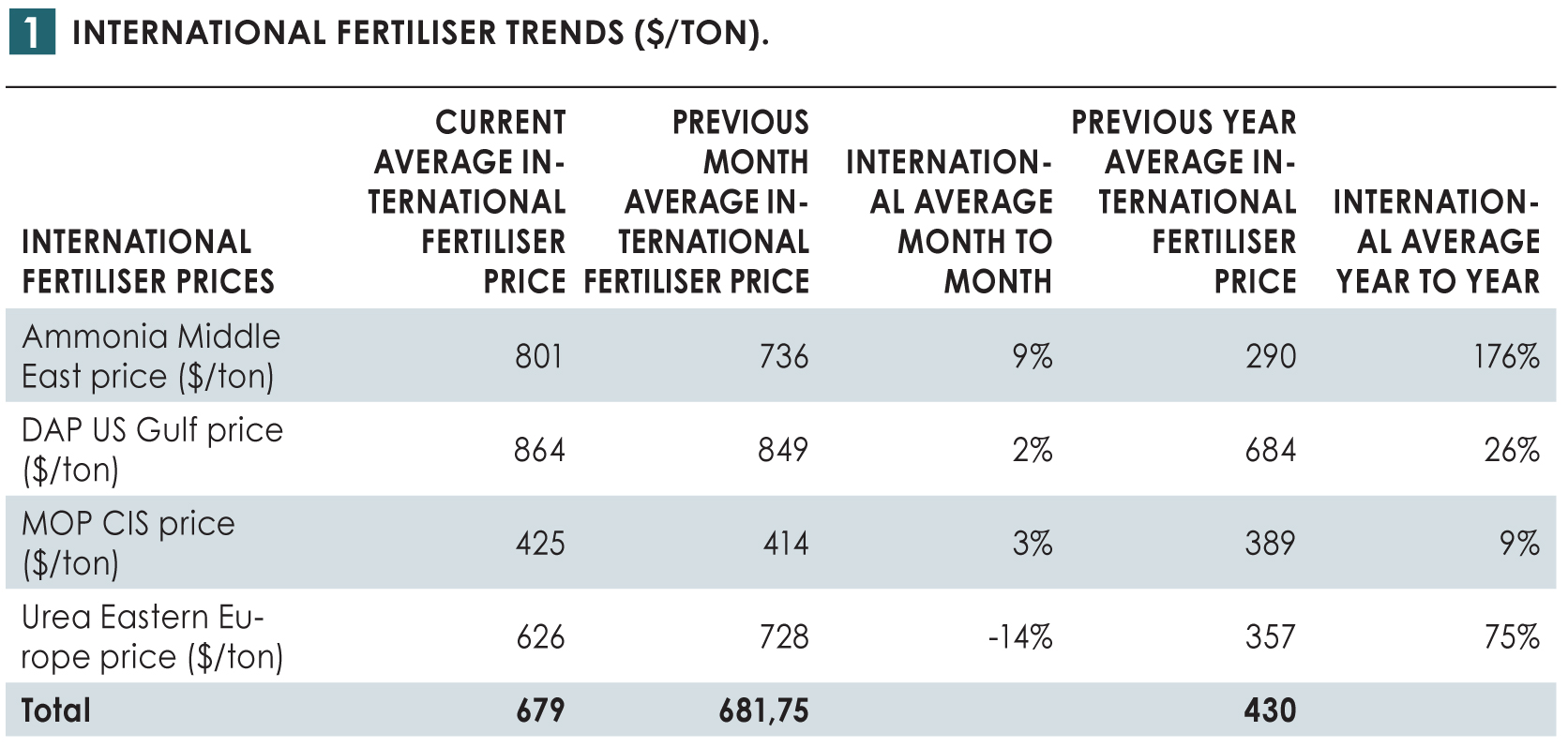

International fertiliser markets show signs of stabilising

The largest price increases were seen at the beginning of the nitrogen fertiliser supply chain. Ammonia prices in the Middle East averaged $801/ton during May 2026, increasing by 9% compared to the previous month and by 176% compared to a year ago. As ammonia prices increased, downstream fertiliser markets also came under pressure. Although urea prices softened during June after reaching exceptionally high levels in May, they remain substantially above last year’s prices. Phosphate fertilisers also continued to increase, supported by higher sulphur prices and ongoing supply constraints.

There are encouraging signs that international markets are beginning to stabilise as shipping through the Strait of Hormuz gradually returns to normal. Improved logistics are easing pressure on global supply chains, while relatively weak demand is helping to soften ammonia and urea markets.

Sulphur, however, remains the key concern. Supply is still constrained, and prices are expected to remain elevated in the short term. Since sulphur is an essential input in phosphate fertiliser production, higher sulphur prices are likely to continue supporting MAP and DAP prices over the coming weeks. This means nitrogen fertiliser prices could ease further if current market conditions persist, while phosphate fertilisers may remain relatively expensive until sulphur supplies improve.

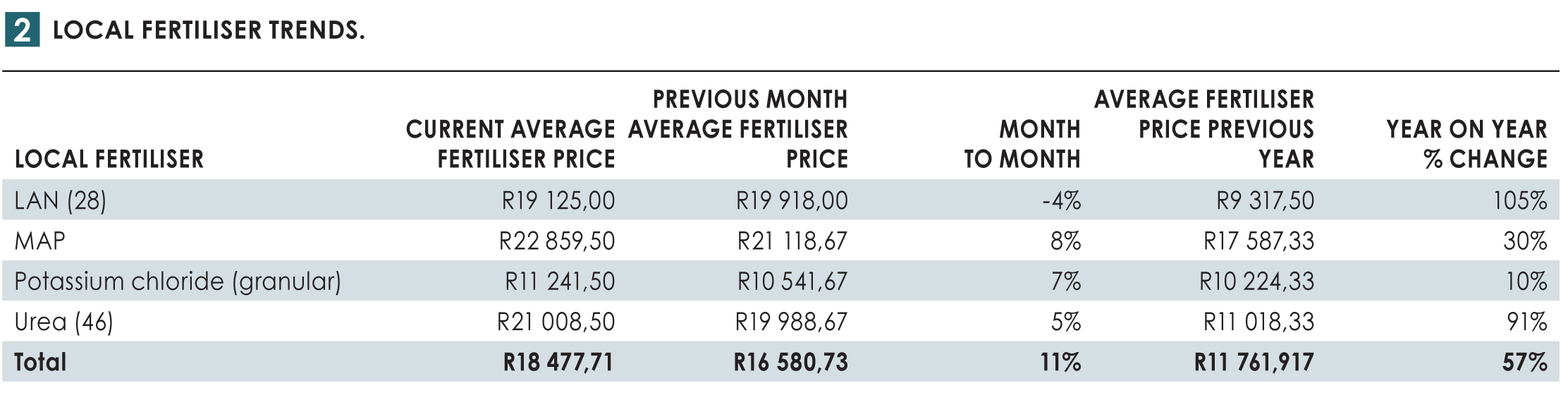

Local fertiliser prices continue to reflect global markets

South African producers have also experienced the impact of these international developments. Changes in global markets are typically reflected in local prices after approximately six weeks as imported products move through the supply chain.

During the past month, LAN prices declined by 4% to an average of R19 125/ton, reflecting some easing in international nitrogen markets. Urea increased by 5% to R21 009/ton and remains approximately 91% higher than a year ago. MAP increased by 8% to R22 860/ton, supported by higher sulphur and ammonia prices, constrained Chinese exports, and earlier shipping disruptions. Potassium chloride (KCl) also increased by 7% to R11 242/ton.

Overall, local fertiliser prices remain approximately 57% higher than a year ago. Although recent monthly movements have been mixed, input costs remain elevated. For summer grain producers, the increase in MAP is particularly significant, as phosphate fertiliser is generally purchased well ahead of planting. If sulphur markets remain tight, producers could continue facing higher phosphate fertiliser costs during the pre-planting period.

The exchange rate also remains an important driver of local prices. During June 2026, the rand traded at an average of approximately R16,42 against the dollar. Because fertilisers are internationally traded in dollars, exchange rate movements directly influence import costs. Fortunately, the relatively stronger rand has helped offset some of the recent international price increases.

Seasonal imports influence local availability

According to SARS trade data, South Africa imported approximately 225 326 tons of fertiliser during the first four months of 2026. Import patterns remain highly seasonal and closely aligned with the summer grain production season. MAP imports generally increase sharply from July onwards, reaching their highest levels during October. Potassium chloride imports typically peak during September, while urea imports show the strongest seasonal trend of all fertilisers, also peaking during early spring in anticipation of increased nitrogen demand. Ammonia imports are less seasonal and appear to be driven more by industrial production schedules than direct agricultural demand.

These seasonal import trends help explain why international market movements often affect local fertiliser prices several weeks later. They also highlight the importance of planning by both suppliers and producers to ensure adequate product availability ahead of planting.

What producers should look for when purchasing fertiliser and lime

While market conditions determine what producers pay, product quality determines the value they receive. The saying “buy cheap, buy twice” is especially relevant when purchasing fertiliser, lime, and gypsum. Under increasing financial pressure, lower-priced products can be tempting, but poor-quality inputs may ultimately reduce crop performance and increase production costs.

To protect fertiliser users, the Fertilisers, Farm Feeds, Agricultural Remedies and Stock Remedies Act (Act No. 36 of 1947) specify allowable tolerances for registered fertiliser and lime products. These tolerances accommodate normal manufacturing variation while ensuring that registered products consistently meet the required quality standards.

When purchasing agricultural lime, producers should pay close attention to three key quality characteristics, including calcium carbonate equivalent (CCE), particle size (fineness) and moisture content.

CCE indicates the lime’s potential to neutralise soil acidity. All agricultural lime products should have a CCE of at least 70%. It is important to note, however, that CCE only reflects the lime’s potential acid-neutralising capacity and does not indicate how quickly it will react in the soil.

Particle size, or fineness, plays a critical role in the effectiveness of agricultural lime. The finer the particles, the greater the surface area available for reaction, allowing the lime to neutralise soil acidity more rapidly.

To comply with quality standards:

- 100% of the lime should pass through a 1,70-mm sieve;

- standard agricultural lime should contain at least 50% of particles finer than 0,25 mm;

- shell lime should contain at least 60% of particles finer than 0,50 mm; and

- microfine agricultural lime should contain at least 90% of particles finer than 0,25 mm, or 80% finer than 0,106 mm.

Moisture content is another important consideration. Excessively wet lime increases transport and handling costs and may affect product quality. The maximum allowable moisture content is 20% for microfine agricultural lime and 15% for standard agricultural lime.

What to do before purchasing or applying fertiliser and lime

To ensure maximum value from every input investment, producers are encouraged to consider the following:

1. Verify that the product is legally registered.

Purchasing only properly registered fertiliser and lime products helps protect crop performance, ensures compliance with quality standards, and reduces production risk.

2. Read the product label carefully.

Confirm that the nutrient composition, manufacturer details, batch number, and application instructions are clearly displayed.

3. Keep accurate records.

Invoices, delivery notes, and product labels are essential in case any product quality disputes arise.

4. Inspect the product before application.

Signs such as damaged packaging, excessive moisture, caking, or contamination may indicate poor product quality and should be investigated before application.

Grain SA members who suspect that a fertiliser or lime product does not comply with its registered label specifications are encouraged to request official product sampling. For more information on the sampling procedure and associated costs, contact Grain SA’s Economic and Member Services Department at economist@grainsa.co.za. Proper product verification not only protects individual producers but also helps maintain quality standards across the agricultural input industry.

In closing, producers should remain alert to market developments and consider both price trends and product quality when making purchasing decisions. Timely procurement and efficient nutrient management will be important tools for managing input costs in the coming season.

{kind=link}