Juan-Pierre Kotzé, manager: Research and Projects, SACOTA

South Africa finds itself in the position of producing yet another record maize and soybean crop. However, despite the large surpluses available for export, deep-sea exports have failed to gain the momentum that many market participants expected at the start of the season. As a result, concerns are growing that if insufficient surplus stocks are exported, South African carry-over stocks will continue to grow, and prices will not resume their typical upward trend in the planting season.

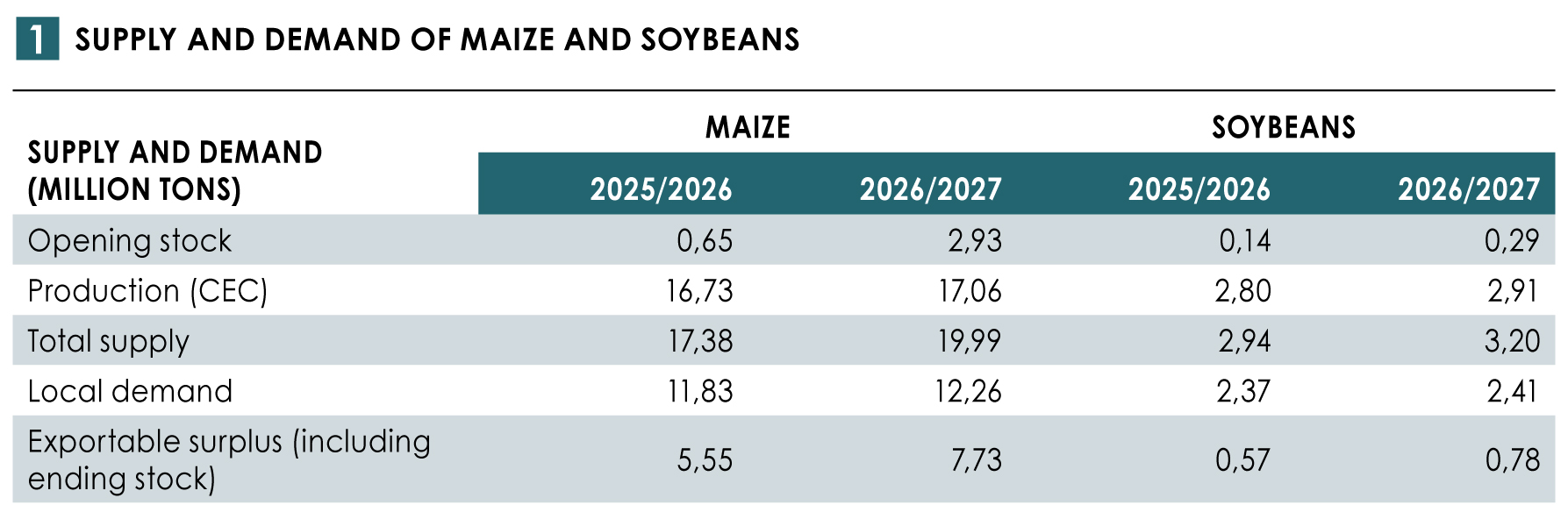

According to the Crop Estimates Committee (CEC) figures released on 26 May, South Africa is expected to produce a record maize crop of 17,06 million tons in 2026/2027. Many analysts expect this number to increase further. Combined with opening stocks of approximately 2,93 million tons and domestic demand (excluding SACU countries) estimated by the National Agricultural Marketing Council (NAMC) at 12,26 million tons (after adjustments such as producer retentions), the country will have a significant exportable surplus of around 7,73 million tons. This is up from the 5,55 million tons of the previous season or 39%.

The NAMC currently projects maize exports of 2,93 million tons during the season, of which approximately 1,73 million tons are expected to be yellow maize, with the balance consisting of white maize. While exports to neighbouring countries continue, many traders argue that these volumes alone will not be sufficient to reduce stocks to comfortable levels. For the market to rebalance, substantial volumes need to be exported overseas.

At the start of the season, slot bookings indicated the potential of exporting around 1,45 million tons. However, at the end of June 2026, it was estimated that only around 550 000 tons of yellow maize would be exported. While the remaining booked slots could potentially accommodate an additional 900 000 tons of exports, some slots have already become commercially unviable due to the timing of international opportunities.

Although the maize situation attracts most of the attention, soybeans face many of the same challenges. The CEC currently estimates soybean production at 2,91 million tons, while many market participants believe that the final crop could exceed 3 million tons, establishing yet another production record. Opening stocks on 1 March 2026 stood at 286 120 tons, while the NAMC projects soybean exports of 280 000 tons. At this stage, no deep-sea export vessels are confirmed. The result is a possibility of significantly larger carryover stocks. The NAMC currently projects soybean ending stocks (28 February 2027) at approximately 468 000 tons, representing a 70% increase from the current season’s opening stock level. While soybeans do not face the same scale of surplus as maize, the underlying challenge remains similar. Without improved export competitiveness, larger stocks are likely to remain within the domestic market.

Although the maize situation attracts most of the attention, soybeans face many of the same challenges. The CEC currently estimates soybean production at 2,91 million tons, while many market participants believe that the final crop could exceed 3 million tons, establishing yet another production record. Opening stocks on 1 March 2026 stood at 286 120 tons, while the NAMC projects soybean exports of 280 000 tons. At this stage, no deep-sea export vessels are confirmed. The result is a possibility of significantly larger carryover stocks. The NAMC currently projects soybean ending stocks (28 February 2027) at approximately 468 000 tons, representing a 70% increase from the current season’s opening stock level. While soybeans do not face the same scale of surplus as maize, the underlying challenge remains similar. Without improved export competitiveness, larger stocks are likely to remain within the domestic market.

The obvious question is why exports are not taking place at the expected pace. The answer ultimately comes down to one factor that influences almost every other aspect of the export programme: the local South African price continues to trade above export parity levels.

Local maize and soybean prices have declined significantly from last year (even from earlier in the season) and are widely regarded as relatively low by domestic standards. However, they remain too high compared to other major global exporters. The three most important maize and soybean exporting countries South Africa competes with are the United States, Brazil, and Argentina. While local yellow maize has managed to secure exports to destinations such as Vietnam, where buyers have been willing to pay a premium for quality, traditional South African markets such as Japan were undercut by the competitors. Argentina and Brazil have large quantities of exportable stocks while the United States had a perfect start to their new planting season in May.

Several factors contribute to this lack of competitiveness. A relatively strong rand has made South African commodities more expensive internationally compared to the recent past. Twelve months ago the rand was weaker against the dollar with exchange rates as high as R18/$, and during mid-2023 (the previous big export season) it was trading at around R19/$.

Rising fuel costs because of the US-Iran war have increased inland delivery costs to the ports. Port and logistics costs remain elevated, while rail inefficiencies continue to force a heavy reliance on road transport.

Importantly, the market does not require the entire crop to trade at export parity levels. Only the part of the crop that has to be exported – perhaps 15% of total production – needs to be priced competitively enough to move into international markets. Once that surplus begins flowing out of the country, domestic supply pressure eases and prices can recover.

However, until that adjustment occurs, the industry faces a difficult reality often summarised by the old market saying: ‘The only cure for low prices is even lower prices.’

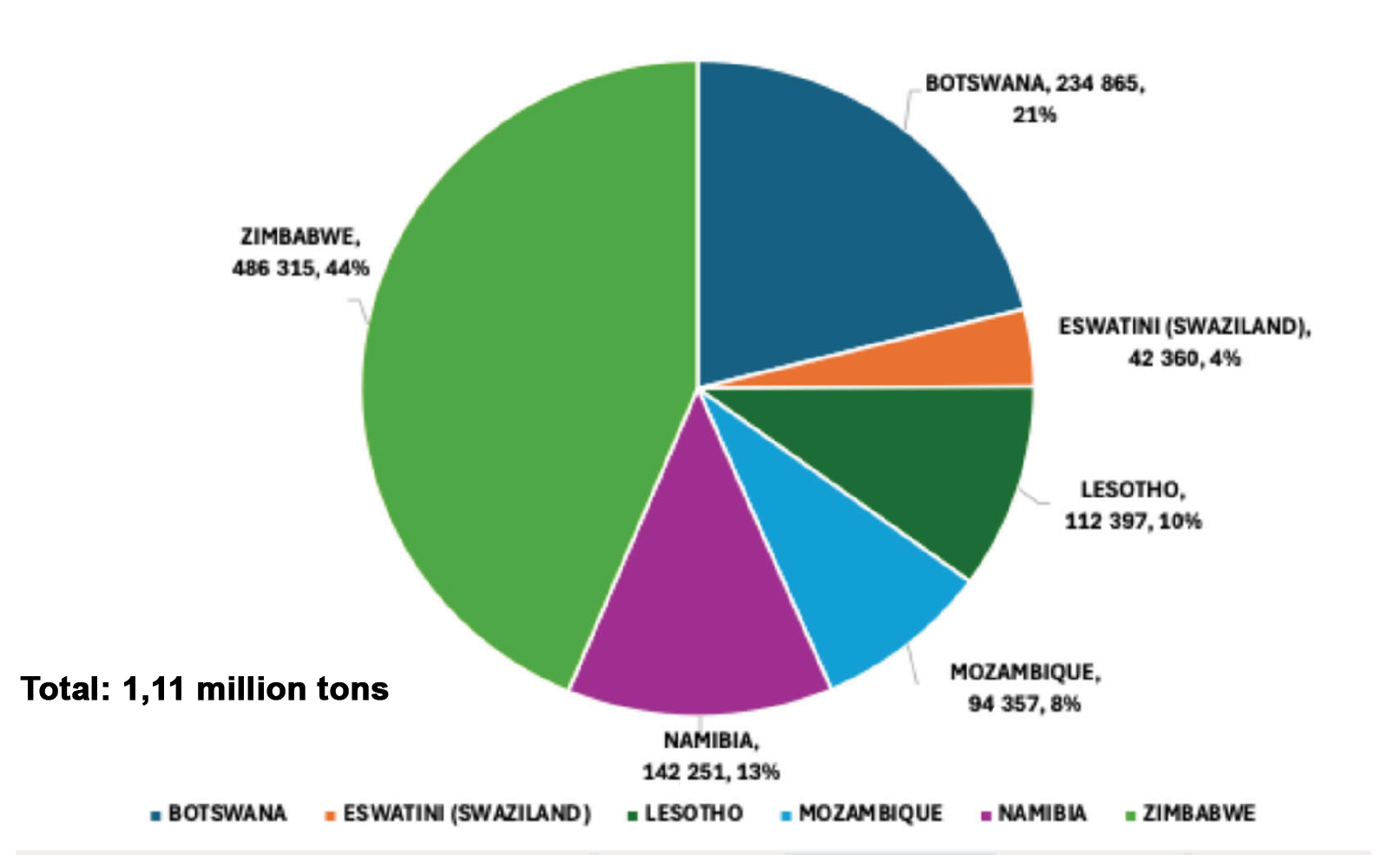

The situation is even more complicated for white maize. South Africa traditionally exports surplus white maize to neighbouring countries, particularly Zimbabwe. This trade is expected to continue, but regional demand alone is unlikely to absorb the available surplus. To make things worse, like South Africa, most of the Southern African countries also had a good production season.

Unlike yellow maize, white maize enjoys limited international demand. In 2023/2024 only 6% or 111 000 tons of total deep-see maize exports were white. Most global markets prefer yellow maize, with limited international markets having a large human consumption component as is the case for South Africa. The last major deep-sea white maize export programme was in 2022/2023 when Mexico ran short of white maize and South Africa exported around 337 000 tons there. Approximately 480 000 tons of white maize were exported to other destinations, including Italy, Honduras, and Korea – totalling deep sea white maize exports of 838 000 tons that season.

Preferably, local white maize needs to trade at a sustained discount to yellow maize in order to encourage greater inclusion in animal feed rations. In turn, this would free up additional yellow maize for possible exports, as South Africa does not have a problem with market access for yellow maize. Although white maize was trading at a discount to yellow maize of around R150/ton (July contract) approximately two months ago, currently the gap has narrowed back to about R60/ton. This is insufficient for profitable inclusion in feed formulations.

Another challenge facing exporters is timing. Global grain markets operate within seasonal windows, and South Africa traditionally enjoys its strongest export opportunity between May and September before major crops from the Americas become available.

This year, however, late harvesting, particularly in soybeans, has created additional complications. Soybeans are ideal to be exported via deep sea before the main maize export programme begins. Port operators generally prefer dedicated export programmes rather than frequently switching between commodities, as this reduces efficiency and increases costs. Ideally, soybean exports would have utilised early-season shipping slots during April and May, before maize exports commenced in June. However, delayed harvesting and uncompetitive pricing prevented any of these opportunities from materialising.

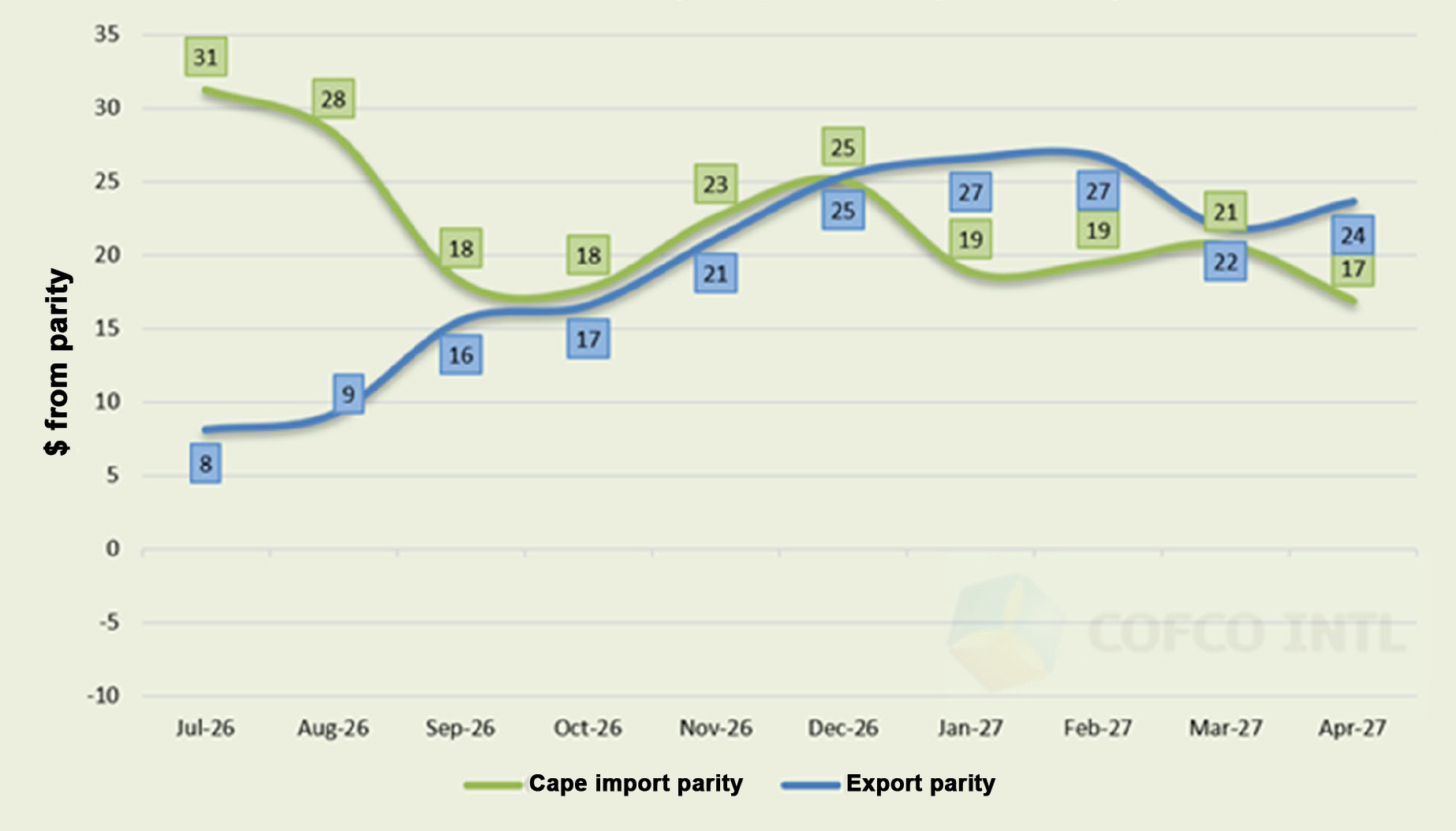

Current estimates suggest that maize remains approximately $8 to $16/ton above export parity, while soybeans are estimated to be around $20 to $25/ton above export parity. As time passes and South Africa moves further away from being competitive on the global export calendar, local prices have to decline even more.

Market participants have also pointed to changing producer behaviour as a contributing factor. Many producers today have greater access to financing and liquidity than previously. This enables them to hold grain for longer periods and reduces the urgency to sell immediately after harvest. Several financiers and their agents are also offering structured finance packages whereby producers can delay pricing their products for several months, the so-called 70-30 package.

Another important factor appears to be the predictions of a super El Niño weather pattern during the next production season. Apparently, many producers have now decided to follow a wait and see approach.

Port selection also influences export profitability and feasibility. While Durban remains the most competitive export route, other ports such as East London and Maputo can reportedly add around $12/ton to export costs. Yet, if South Africa is to export the large surpluses currently available, these alternative routes may also be required, especially taking into account maize and soybeans that would need to be exported simulta-

neously. The more expensive the export route, the lower the commodity price must be to make exports commercially viable. What appears to be a competitive road transport cost to the port, could also evaporate quickly if there are delays in truck turnaround times.

Market participants also continue to debate issues such as JSE transparency and the effectiveness to accurately reflect market conditions. While opinions differ, these factors may also influence the speed at which the market adjusts to current supply realities.

Although the South African Cereals and Oilseeds Trade Association (SACOTA) expects more maize and soybeans to come to the market in the next two to three months, it is debatable whether the volumes will be sufficient to drive prices low enough to secure new export deals. Only time will tell.

For more information contact Dr André van der Vyver (andre.vandervyver@sacota.co.za) or Juan-Pierre Kotzé (info@sacota.co.za).

{kind=link}