South Africa’s grain and oilseeds industry stands at a crossroads of global technological innovation and local trade regulations might create some trade barriers regarding food security of crucial crops like wheat. Agricultural technology globally is changing rapidly with new breeding techniques (NBTs) gaining traction internationally. South Africa’s uniquely cautious regulatory framework could cause the country to fall behind in terms of production efficiency and presents potential trade barriers, especially given its heavy reliance on wheat imports.

What are NBTs?

NBTs encompass modern genomic tools that allow breeders to make precise genetic changes in crops. According to an article by the European Parliament (2 February 2024), many NBT products, unlike traditional transgenic genetically modified organisms (GMOs), contain no foreign DNA and can be indistinguishable from variations that occur naturally or through conventional breeding methods.

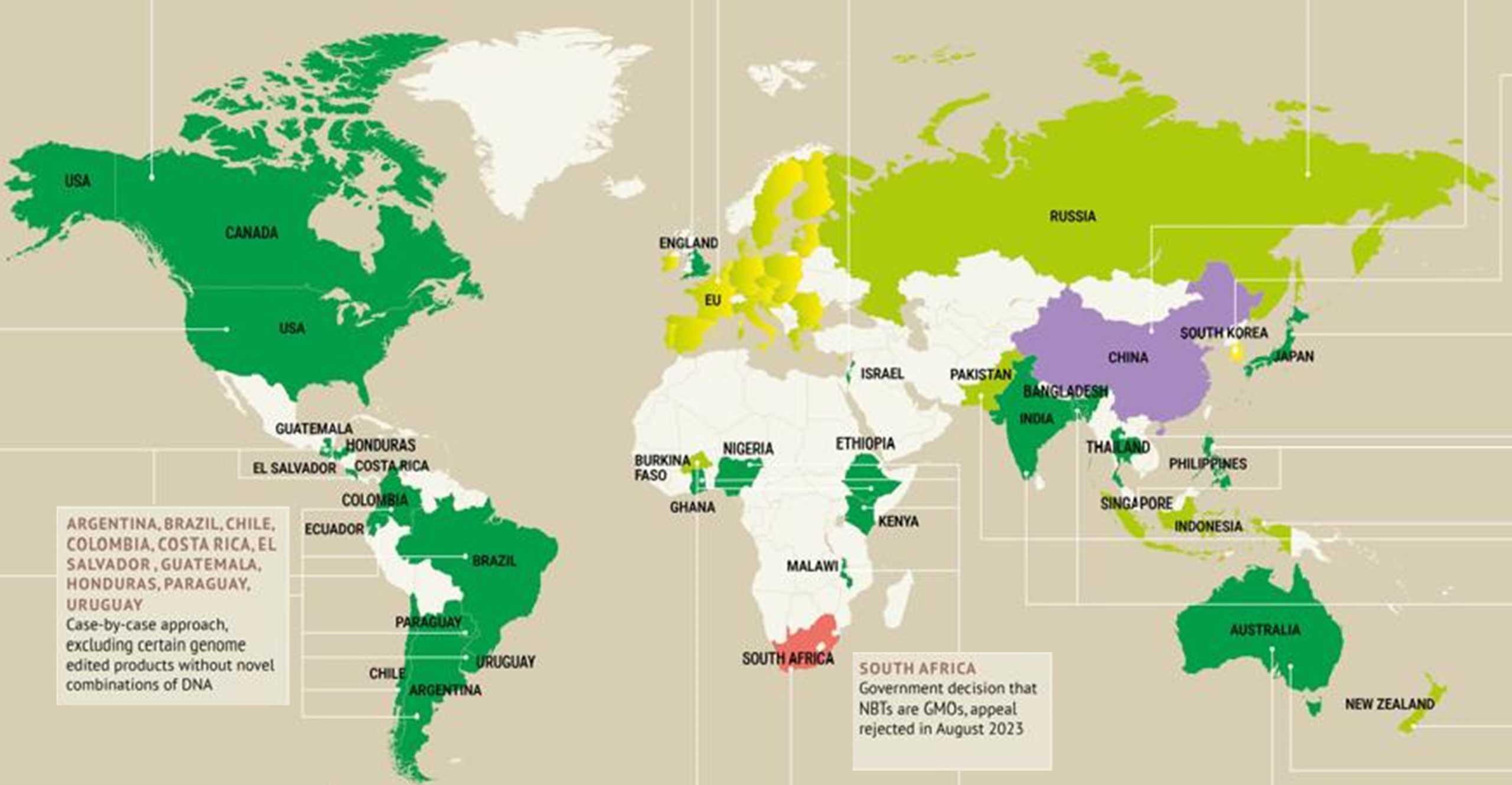

Globally, several countries have adapted regulatory systems to treat certain NBT products differently from traditional GMO crops, particularly when edits could have occurred through natural mutation or conventional breeding. Such product-based regulatory approaches where the characteristics of the end product determine oversight, are being adopted in nations such as Brazil, Argentina, the United States, Japan, and others (ISF, 2025).

However, South Africa remains the only jurisdiction to explicitly state that all products derived from NBTs will be regulated entirely under the existing Genetically Modified Organisms Act (the GMO Act No. 15 of 1997). This was clarified by the Department of Agriculture (previously known as DALRRD) in 2021, confirming that the extensive risk-assessment processes and approval pathways required under the GMO Act will apply to NBTs. This decision was then appealed, but the appeal got rejected in 2023.

SA’s wheat market: import dependence and trade patterns

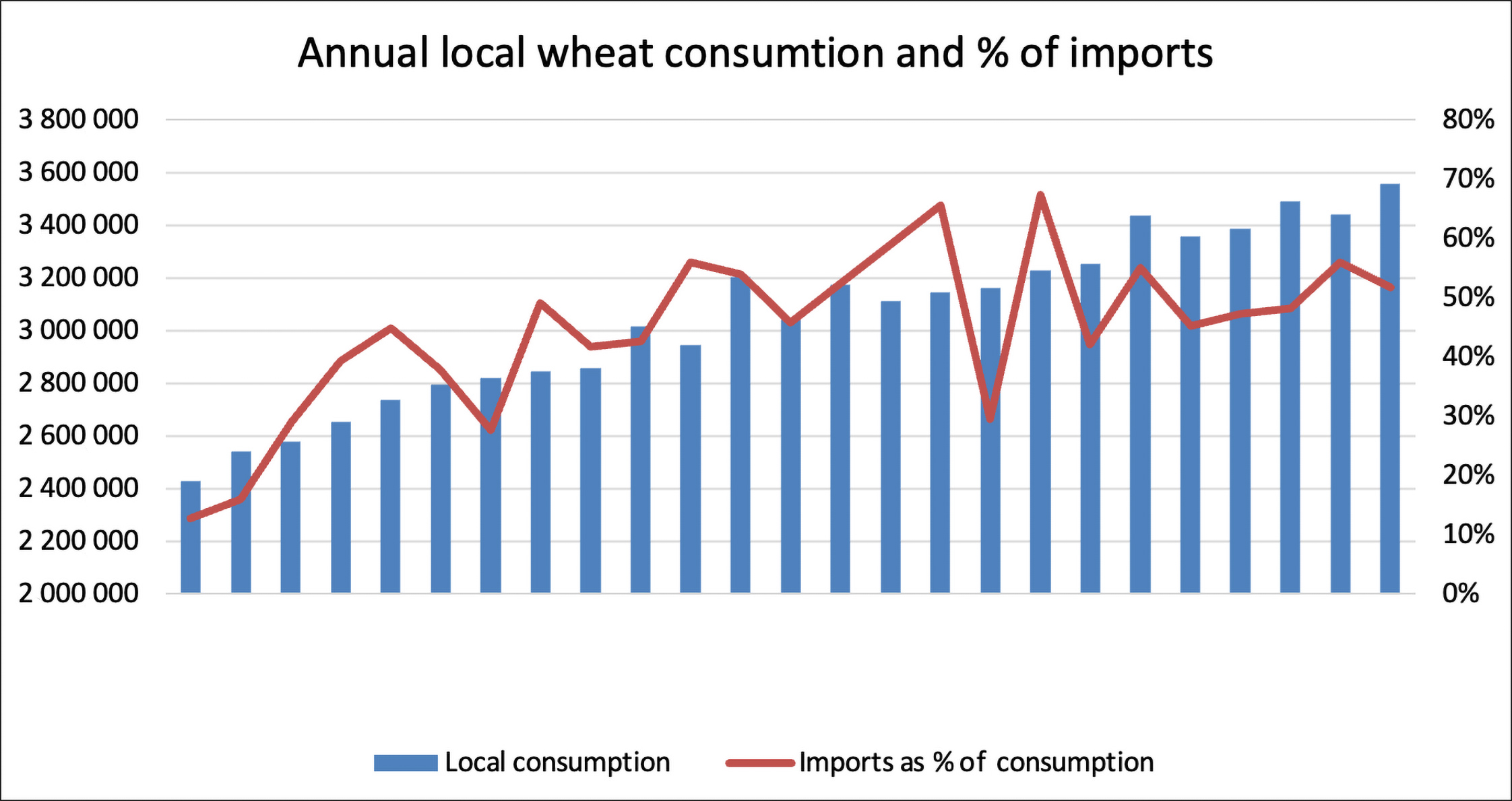

South Africa is a net importer of wheat, importing roughly half of its annual consumption needs each year due to the gap between domestic production and demand. Estimates for the 2025/2026 marketing year suggest total wheat imports of approximately 1,75 million tons to supplement local supplies, against total consumption of around 3,56 million tons.

The country has seen a decrease of around 18% in the production of wheat since the year 2000, while also increasing the local consumption with about 45%. The difference needs to be imported to ensure food safety for South Africa. The need to import wheat is increasing, making the importance of policy synchronisation with other countries crucial for the South African market.

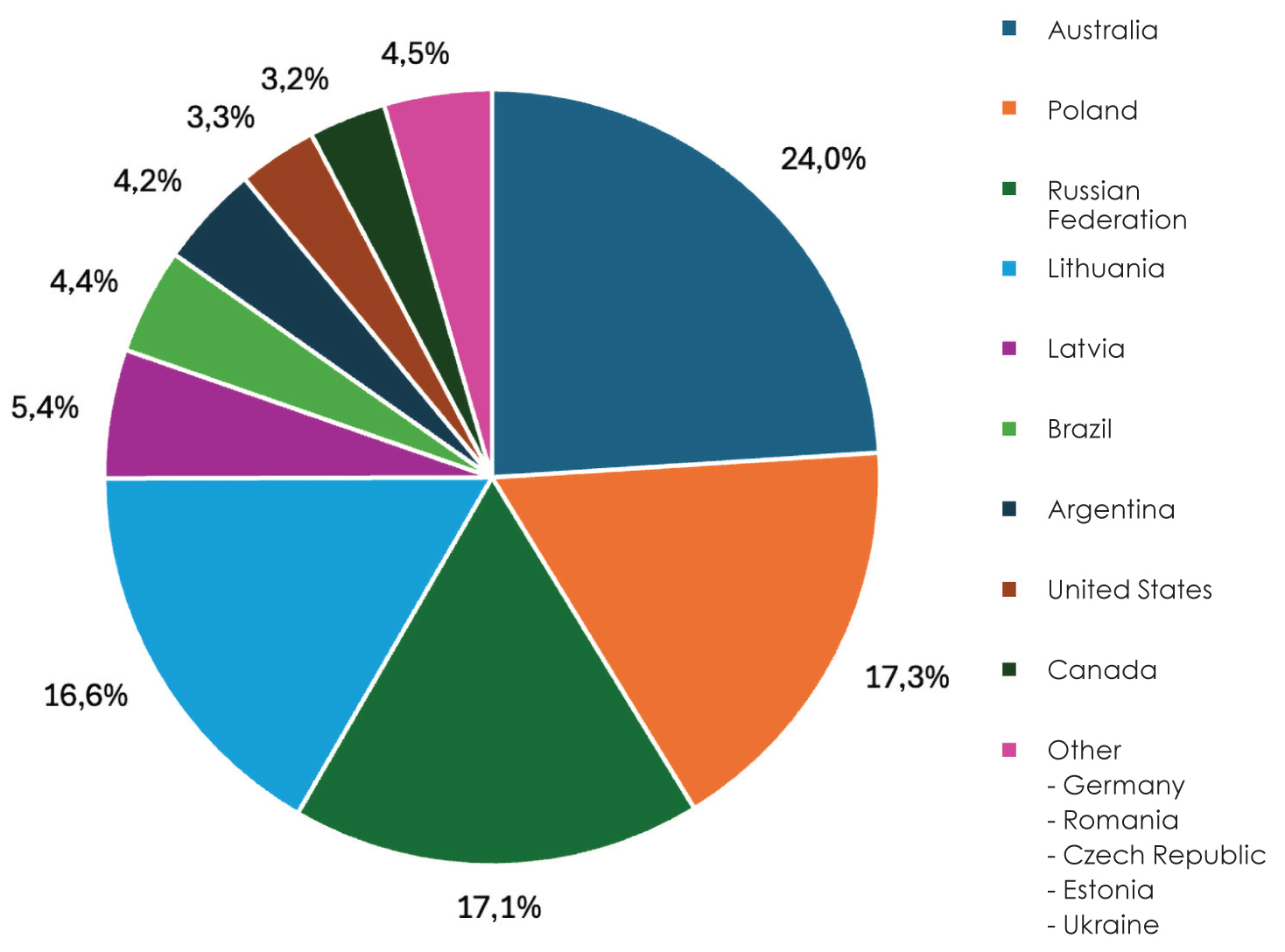

Major supplying countries in recent years have included Australia, Lithuania, Poland, and Russia; preference and arrival patterns vary due to the harvesting time per country as well as global price trends.

Although South Africa has a variable import tariff (currently R619,00/ton) to protect the local production market, this tariff can’t work in isolation. Synchronising the policy and regulatory frameworks in South Africa with that of other countries will also enable local wheat producers’ access to these NBT technologies to potentially increase their productivity and therefore profitability. This policy decision is therefore affecting the wheat industry and other agricultural industries throughout the value chain.

Source: International Seed Federation (2025)

Regulatory synchronisation and potential trade barriers

South Africa’s import regime for GMOs is governed by legally mandated lists of approved GMO events for commodity use and general release, against which all imports must be assessed. Any GMO intended for import must appear on South Africa’s list and must be synchronised with the list of approved events in the country of origin. This means the country of origin should not have any GMO approved events for cultivation on their list that does not appear on the South African list.

This creates a potential trade problem if a major wheat-producing country treats an NBT wheat variety as a non-GMO or conventional variety under its own laws. This will in turn mean that this product would not be registered or listed as a GMO in the country of origin and will complicate the process of synchronisation. Under current South African legislation, such a product could not be legally imported, even if it is treated as a conventional variety elsewhere. This could constrict the supply of wheat from key producers who utilise NBT technology but do not regulate it as a GMO.

Argentina provides a real-world example. According to an article by Neocrop (developer of a gene-edited wheat variety) in September 2025, Argentina’s National Advisory Committee on Agricultural Biotechnology (CONABIA) declared the gene-edited high-fibre wheat cultivar as ‘non-GMO’ and therefore it will not be regulated under their GMO regulations. This wheat variety is effectively being treated as conventional wheat. Field trials with this high-fibre wheat variety have started in Chile, and are also expected to commence in Argentina in the coming season to evaluate the variety in ‘real-world’ conditions. Even though this variety is not yet available commercially, Neocrop have started discussions with milling and baking stakeholders to commence a pilot project to enable them to start multiplication of the seed.

If this NBT wheat were to become commercially available, the lack of GMO classification in the country of origin could prevent South African authorities from approving imports under existing regulations. South Africa has received 360 000 tons of wheat from Argentina in the past five years. Although this is a small percentage of the total imports, having this market open remains important to ensure food security. Chile and Argentina are leading the way for field trials on NBT wheat, but other major producing countries will follow suit soon after.

Similar dynamics would emerge with other major exporters that adopt product-based rather than process-based regulatory systems. As such, South Africa risks developing asynchronous regulatory standards that act as non-tariff barriers, restricting market access for new wheat types that are considered conventional in international markets.

Broader issues with asymmetric regulation

Experts and industry groups in South Africa have raised concerns that automatically classifying NBT products as GMOs may impose unnecessary economic burdens on both domestic breeders and international trade partners. Because NBT-derived crops often require the same extensive dossiers, risk assessments, and approvals as traditional GMOs, innovators may face higher compliance costs, extended delays, and limited adoption, potentially disadvantaging South African agriculture relative to global competitors.

Trade dynamics are further complicated by the fact that many importing countries have different regulations between GMO and NBT products, which may diverge significantly from South Africa’s framework. This regulatory asymmetry could not only affect wheat imports but also the broader agricultural supply chain including exportation of South African maize and soybeans once NBT technologies are approved for such products.

Other countries, as is the case for South Africa, require synchrony of GMO products between trading countries. If South Africa were to add a NBT product (for example maize) to the approved general release list, this will allow South African producers to commercially use this NBT product. If the destination country’s regulation does not regulate NBTs in the same manor, they could potentially refuse a shipment due to the asynchrony that this product on the South African list causes. Strictly speaking, when declaring our list of GMO-approved events, the NBT product should not appear on that list.

Conclusion

For South Africa, with its substantial wheat import dependence and exposure to global market shifts, it is critical to align regulatory approaches with key trade partners. Without regulatory synchronisation the country risks excluding quality wheat supplies that emerge from NBT breeding programmes abroad, potentially raising costs for consumers and the entire value chain while making access to new technology more difficult to South African producers.

1 Product-based regulation in terms of NBTs refers to regulation that is based on the final product, whereby, if the genetic changes could have occurred naturally or through conventional breeding it would be regarded outside of the GMO regulation.

2 Process-based regulation in terms of NBTs is regulation based on the process used, whereby, if any modern biotech method was used to alter the DNA of a product, it would be regarded as a GMO product, irrespective of the final product.

{kind=link}